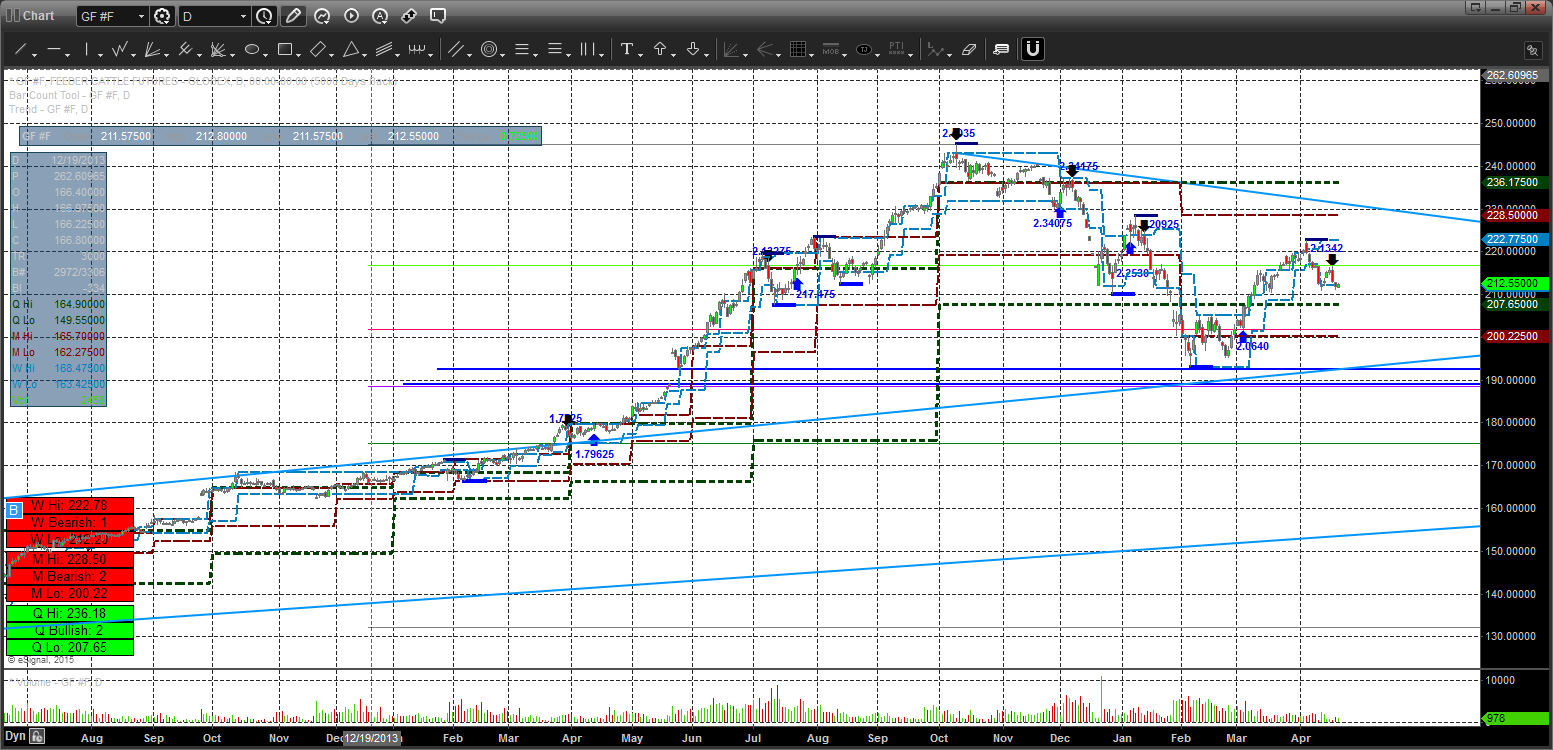

Feeder Cattle went short in the April (J5) contract at 2.1342. I sold the May futures, given April goes off the board next week. When a commodity is demonstrating a behavior consistent with either a seasonal or contra-seasonal cyclical pattern, any (statistically proven) trend system can be used to time the seasonal inflections to enhance alpha generation. All markets are inherently cyclical; the periodicity of inflection ‘months’ (associated with seasonal cycles) act as a discretionary indicator, whereby program signals can be ‘scored’ or valued based on their monthly occurrence – inline with the seasonals. In the case of Feeder Cattle, the market is trading seasonally in 15′ – trending higher into the Spring — lower into the summer — higher into the fall (to be expected). When we develop that seasonal insight, use a reliable trading tool to time the entry/exit algo coordinating with anticipated monthly reversals. I watched Feeder Cattle struggle at the 2.20$ level, then pivot and generate a sell signal. Although trade location is not ideal, I’m leaning on the seasonal to pressure the market into summer lows. If my system generates a fresh long between now and Aug, there would be 2 ways to approach this: Take the long entry if the exposure warrants an acceptable amount of risk and at fractional unit sizing or do not buy the market unless the signals presents closer to the seasonal timing (Buy a long entry in late July/Aug). Quarterly support on the continuous contract (attached) (green dashed line) stands at 2.0765, with Monthly time frame of support at 2.0025 (brown line). The downside looks reasonably contained here, structurally in the May contract.